GFI: Egypt lost US$1.6 billion to Trade Misinvoicing in 2016; Revenue needed for SDGs

July 16, 2019

By Ben Iorio

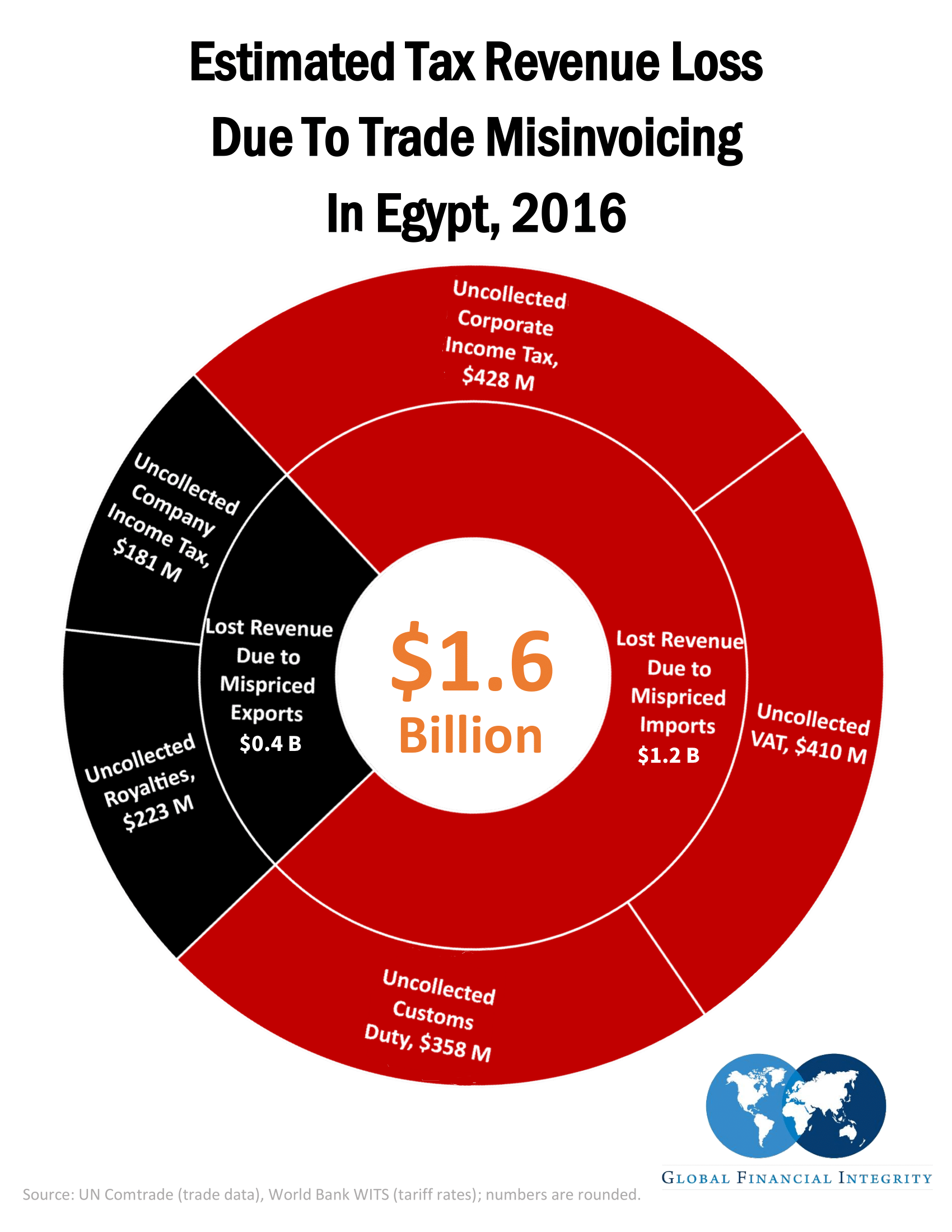

On June 26th, Global Financial Integrity (GFI) published a comprehensive study estimating Egyptian revenue losses of approximately US$1.6 billion as a result of trade misinvoicing in 2016. By deploying a detailed analysis of the United Nations Comtrade database (Comtrade), GFI was able to estimate the government revenue losses of approximately US$1.6 billion, or 4.1 percent of Egypt’s total government revenue collections in 2016. GFI concluded its report by recommending both national and international policy initiatives the Egyptian government can take to curtail illicit financial flows and regain revenue lost to trade misinvoicing.

What is Trade Misinvoicing?

Trade misinvoicing is the act of exploiting global trade as a way to avoid customs duties, value added taxes (VAT) or corporate income taxes, fraudulently access subsidies, or hide illicit cash flow. Trade misinvoicing occurs when one side of a trade mis-reports either the quantity, price, or quality of the goods being traded and can take on four forms- import over-invoicing, import under-invoicing, export over-invoicing and export-under invoicing. These practices result in government revenue losses and, depending on the type of misinvoicing, illicit inflows and outflows to/from a country.

For example, if China reports a shipment of US$3 million worth of plastics to Egypt, but Egypt only reports US$2 million worth of plastics received from China, then either the exporter on the Chinese side has committed export over-invoicing, or the importer on the Egyptian side has engaged in import under-invoicing. This could be done as a way to launder money into Egypt, or to avoid paying corporate income taxes on the importing side. Trade misinvoicing is easily preventable using tools like GFI’s GFTrade, which tracks recent trade prices across major trading countries, enabling customs officials to check invoices for fraud in real time.

Methodology

By analyzing the export data of all trade partners with Egypt, as well as Egypt’s import data from Comtrade, GFI was able to estimate the overall trade gap between what Egypt reports as having exported/imported, and what its trading partners report as exporting/importing to/from Egypt.

GFI estimated that the value of the trade gap for misinvoiced goods in Egypt was roughly US$8.5 billion, or 10.5 percent of its total trade of US$80.6 billion in 2016. To estimate the revenue losses Egypt may have incurred, GFI analyzed existing VAT taxes, customs duties, royalties and company income taxes, applying these rates to the transactions where trade misinvoicing occurred.

Next, GFI examined the HS product codes to determine what types of goods were most frequently misinvoiced and from which countries they originated. The Egyptian imports most at risk for high values of import under-invoicing were essential oils, vehicles, machinery and meats, while the countries with the highest values of import under-invoicing were Ireland, China and Switzerland.

Lost Development Spending from Trade Misinvoicing

The US$1.6 billion Egypt is estimated to have lost to misinvoicing in 2016 is money that could have been spent advancing Egypt’s progress on the internationally agreed-upon Sustainable Development Goals (SDGs).

An additional US$1.6 billion in revenue could have been spent in a way that mirrored previous United Nations Development Programme (UNDP) spending in Egypt. Previously, UNDP spending in Egypt was allocated to approximately 32 percent for No Poverty (SDG 1), 32 percent for Decent Work (SDG 8), 13 percent for Peace, Justice and Strong Institutions (SDG 16), 9 percent for Life on Land (SDG 15) and 5 percent for Climate Action (SDG 13), with the remaining 9 percent divided among the remaining SDGs. Allocating an additional US$1.6 billion in this way could have resulted in US$512 million more for No Poverty (SDG 1), US$512 million for Decent Work (SDG 8), US$208 million for Peace, Justice and Strong Institutions (SDG 16), US$144 million for Life on Land (SDG 15) and US$80 million for Climate Action (SDG 13), with an additional US$144 million for the remaining SDGs.

Other possibilities for spending the lost US$1.6 billion could have included an increased focus on hunger, education and decent work. In June 2018, the World Bank published a paper entitled ‘Sustainable Development Goal Diagnostics: The Case of the Arab Republic of Egypt’, finding that Egypt had seen improvement in nine of the reported 15 SDGs. Of the SDGs that did not see improvement were Zero Hunger (SDG 2), Education (SDG 4), Decent Work (SDG 8), Sustainable Cities and Communities (SDG 11) and Responsible Consumption and Production (SDG 12). The report also noted that, “despite the fact that the eradication of extreme poverty has been statistically achieved, it is one of increasing importance to prioritize the needs of those living below the poverty line.”

Based on such concerns, Egypt could have used the resources lost to trade misinvoicing for increased spending on Quality Education by an additional US$720 million (SDG 4); on Decent Work and Economic Growth by an additional US$352 million (SDG 8); on Good Health and Well-Being by an additional US$304 million (SDG 3) and on Sustainable Cities and Communities by an additional US$208 million (SDG 11). Such additional spending on these sectors could have greatly benefited those in poverty and aided Egypt’s efforts to achieve its SDGs by the 2030 deadline.

Global Financial Integrity’s Policy Recommendations to Egypt

Domestically, Egypt could:

- Increase Penalties for Customs Fraud – Egypt’s legislation that addresses trade misinvoicing is its Customs Law No. 66 adopted in 1963. Currently Article 118 imposes a fine that equals one quarter of the customs duty for providing incorrect data on the origin and type of goods. Articles 121 and 122 state, “Submitting false and fabricated documents of invoices” is a form of smuggling that can be punished by imprisonment or a fine of not less than five hundred pounds (US$30) and not exceeding ten thousand pounds (US$600). GFI recommends that Article 122 be amended so that the penalty equals the amount of the customs duty that would have otherwise been lost, plus an additional penalty for filing false documents.

- Increase Customs Resources – In 2008, the Egyptian customs department established a risk management system alongside USAID to streamline the goods declaration processes. While this aids the process of declaring goods, a risk-assessment tool like GFI’s GFTrade could further enhance the Egyptian government’s ability to prevent trade misinvoicing in the future and thereby increase tax revenue for Egypt. Designed by GFI to build the capacity of customs authorities to better detect misinvoicing as transactions are occurring and take corrective steps in real time, GFTrade allows for real-time price comparisons of goods by drawing upon reported price data over the previous twelve months. Using GFTrade, customs officials can flag invoices with unusually high or low prices for further investigation. Increasing customs resources could help Egypt prevent future revenue losses due to trade misinvoicing, and help the country crack down on illicit financial flows and increase its development budget in the process.

Internationally, key areas of importance include:

- Beneficial Ownership – GFI recommends that Egypt consider making its existing beneficial ownership legislation (requirements that the true owners of companies are disclosed) part of its customs law and that it takes steps to encourage all governments to establish public registries of beneficial ownership information.

- Anti-Money Laundering – In May 2009, Egypt became a member of the Middle East and North Africa division of the Financial Action Task Force (FATF), which works to combat money laundering and terrorist financing. GFI commends Egypt for this, and recommends Egypt encourage all governments to adopt and fully enforce FATF’s anti-money laundering recommendations and existing anti-money laundering legislation.

- Country-by-Country Reporting – In 2018, Egypt implemented country-by-country reporting. GFI commends Egypt for this action, and recommends Egypt encourage other governments to require multinational companies to publicly disclose their revenues, profits, losses, sales paid, subsidiaries and staff levels on a country-by-country basis.

- Tax Information Exchange – Egypt joined the Global Forum on Transparency and Exchange of Information for Tax Purposes in 2016. However, Egypt has not yet set a date for its first automatic exchange of information. GFI recommends Egypt set a date and encourage all governments to actively participate in the worldwide movement towards the automatic exchange of tax information as endorsed by the Organization for Economic Cooperation and Development and the G20.

- Addis Tax Initiative – Egypt has not officially signed on to support the Addis Tax Initiative, which supports transparency, fairness, efficiency and effectiveness within tax systems. GFI recommends Egypt consider signing on to the Addis Tax Initiative and encourage other governments to do the same, in an effort to further curb illicit financial flows.

Read the full report here.

Ben Iorio is a 2019 GFI Summer Intern and a student in Economics at the University of Michigan.