Trade Misinvoicing

Trade misinvoicing is a method for moving money illicitly across borders which involves the deliberate falsification of the value, volume, and/or type of commodity in an international commercial transaction of goods or services by at least one party to the transaction. Trade misinvoicing is the largest component of illicit financial outflows measured by Global Financial Integrity. Explore our most recent data on trade misinvoicing here.

By fraudulently manipulating the price, quantity, or quality of a good or service on an invoice submitted to customs, criminals can easily and quickly shift substantial sums of money across international borders.

Trade misinvoicing can be related to, but does not precisely correspond to, trade-based money laundering (TBML). Rather, trade misinvoicing is mechanism that can be used to engage in TBML. The Asia/Pacific Group on Money Laundering defines TBML as “the process of disguising the proceeds of crime and moving value through the use of trade transactions in an attempt to legitimize their origins.”

Why is Trade Misinvoicing Used?

Broadly, there are four primary reasons to misinvoice trade:

Broadly, there are four primary reasons to misinvoice trade:

- Money laundering: Criminals or kleptocrats may seek to launder the proceeds from crime or corruption.

- Directly evading taxes and customs duties: By under-reporting the value of goods, importers are able to immediately evade substantial customs duties or other taxes. Additionally, under-reporting the value of exports also allows companies to understate their revenues, and in turn, reduce their income tax liability.

- Claiming tax incentives: Many countries offer generous tax incentives to domestic exporters selling their goods and services abroad. Criminals may seek to abuse these tax incentives by over-reporting their exports.

- Dodging capital controls: Many developing countries have restrictions on the amount of capital that a person or business can bring in or out of their economies. Individuals or entities attempting to break these capital controls often misinvoice trade transactions as an illegal alternative to getting money in or out of the country.

As many countries attempt to process customs transactions quickly, in an effort to promote trade and boost economic growth, trade misinvoicing has become a fairly low-risk endeavor for criminals—especially those who only moderately misinvoice their transactions by, say, 5 to 10 percent.

How Does Trade Misinvoicing Work?

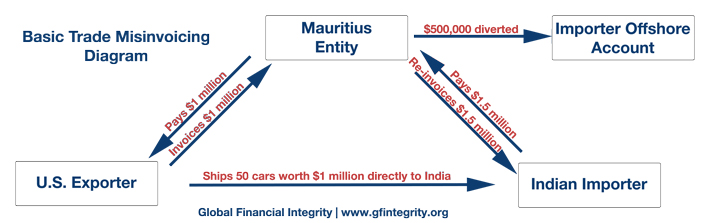

Consider the following diagram:

In this case of import over-invoicing, the Indian importer illegally moves $500,000 out of India. Although he is only buying $1 million worth of used cars from the U.S. exporter, he uses a Mauritius intermediary to re-invoice the amount up to $1,500,000. The U.S. exporter gets paid $1 million. The $500,000 that is left over is then diverted to an offshore bank account owned by the Indian importer.

GFI’s methodology would pick up this transaction as an illicit outflow of $500,000.

What about Tax Avoidance by Multinational Companies?

Because they often both involve mispricing, many aggressive tax avoidance schemes by multinational corporations can easily be confused with trade misinvoicing. However, they should be regarded as separate policy problems with separate solutions.

That said, multinational corporations can and do engage in trade misinvoicing. This activity, however, involves the deliberate misreporting of the value, volume, or type of commodity in a customs transactions, and is thus illegal tax evasion, not legal tax avoidance.